Developer Tool Ecosystem

This post is a written companion to a slide deck I put together in November 2023 -- a thesis on the SaaS and developer tool ecosystem. The full 6-pager is available to download below. Download the full deck (PDF) ->

The developer landscape

Developers are becoming the most important buying unit in enterprise software. Not IT. Not the CTO alone. The individual developer.

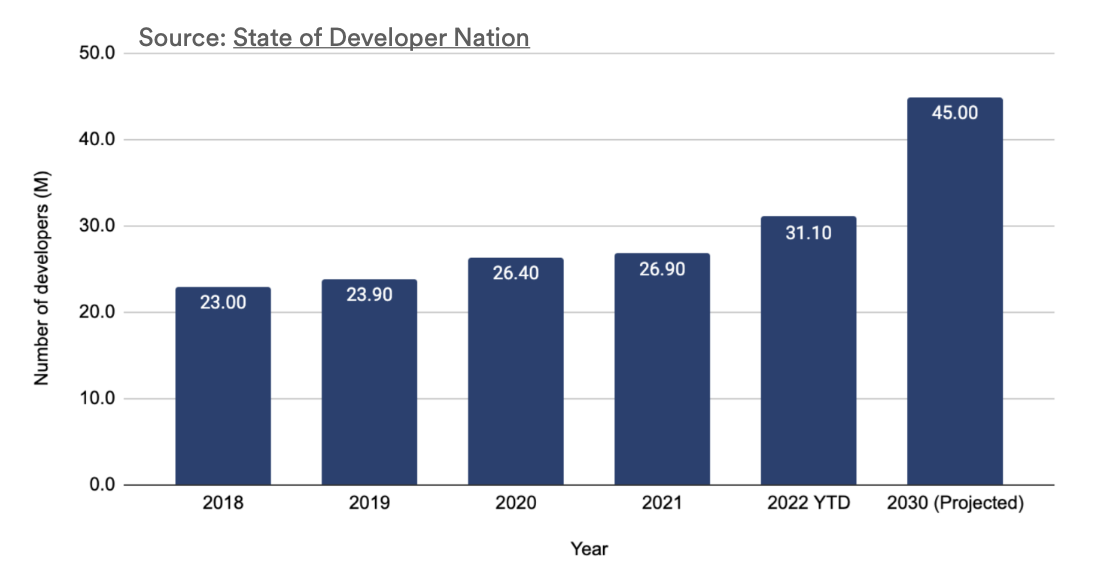

Developer count growing at 5-6% annually. Source: State of Developer Nation

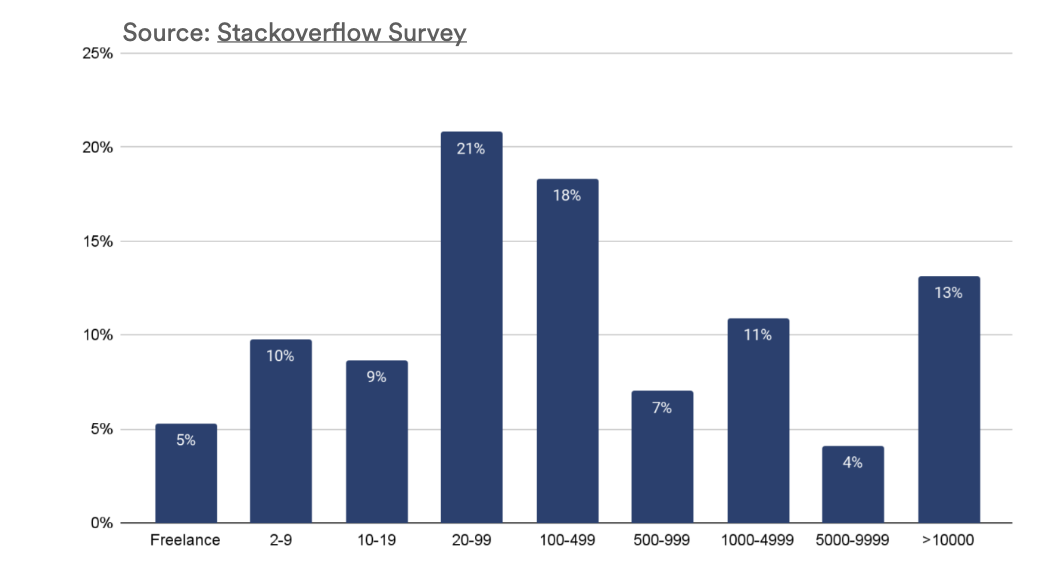

More than 58% of developers work at companies under 500 employees -- small teams with no bandwidth to build internal tooling. Source: Stack Overflow Survey

What makes developer tools structurally different from other SaaS: the buyer and the user are the same person. No procurement committee, no lengthy evaluation cycle. A developer tries a tool, it works, it spreads. Or it doesn't, and they move on in an afternoon.

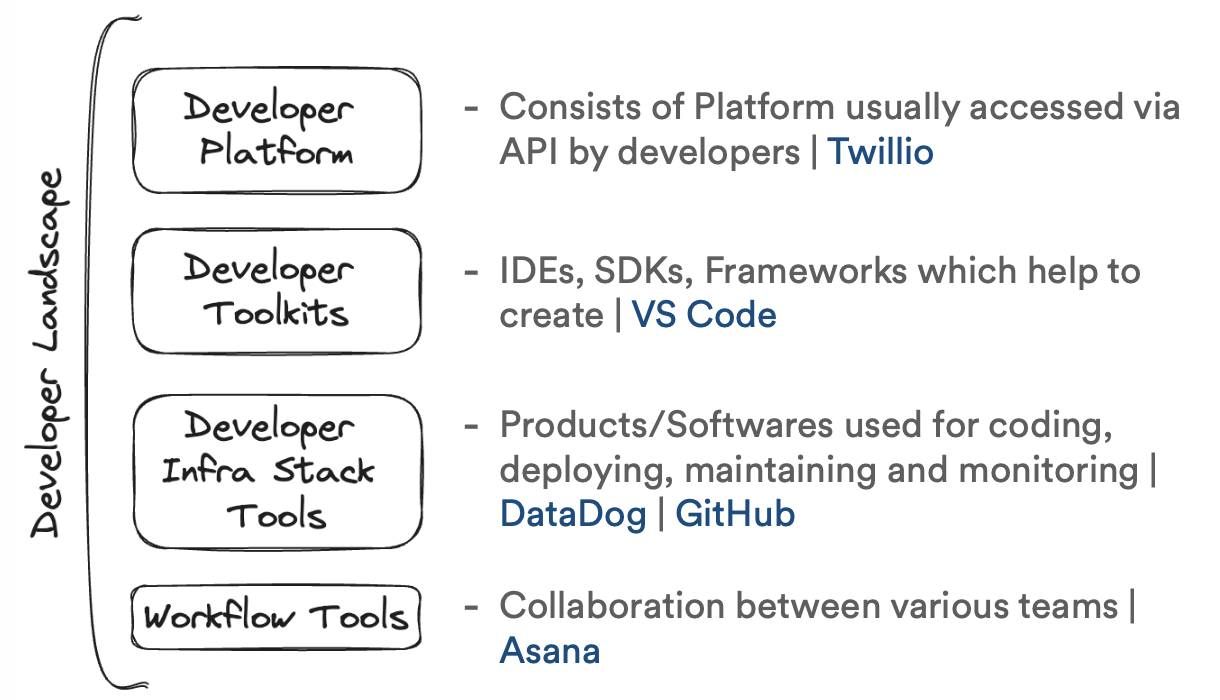

The developer landscape breaks into four categories:

Developer Platforms (API-accessed, like Twilio), Toolkits (IDEs, SDKs, like VS Code), Infra Stack Tools (deploy, monitor, like GitHub and DataDog), and Workflow Tools (collaboration, like Asana).

As companies stay smaller for longer and internal engineering bandwidth stays constrained, the market for tools in each of these four categories only expands.

How many tools, and why aren't they free?

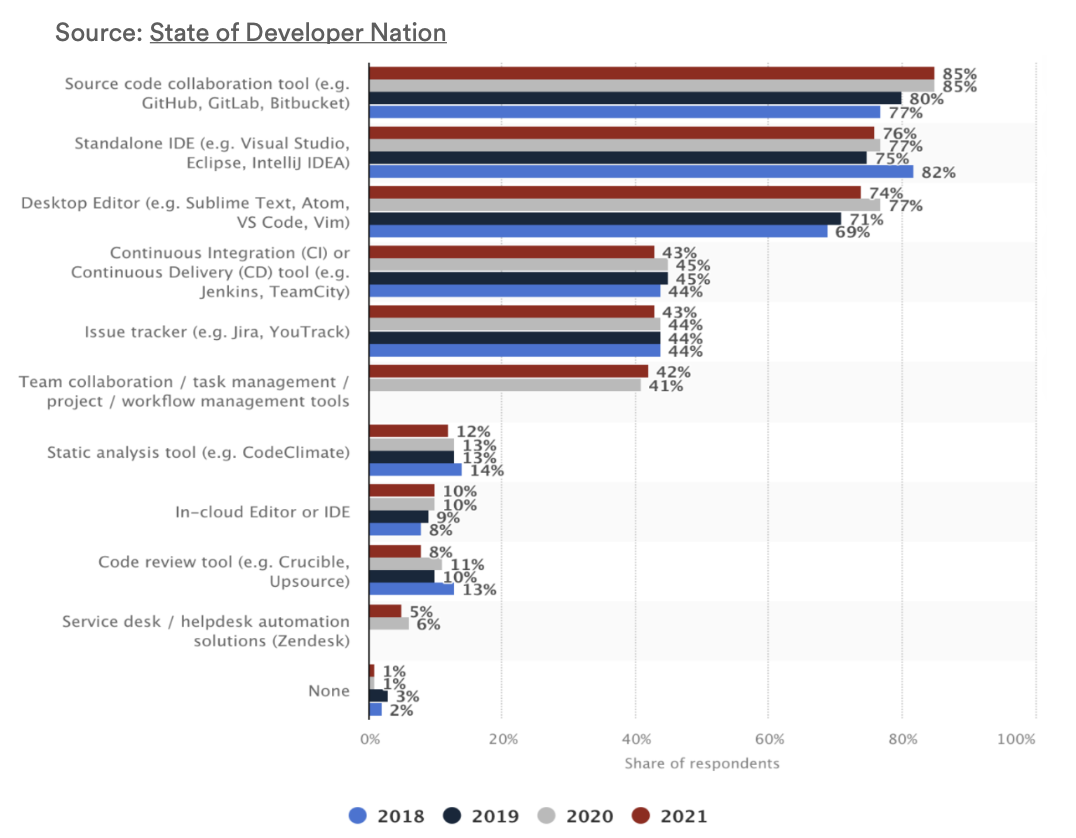

Developers use at least 4 tools on average. Version control is near-universal at 80-85%. IDEs, desktop editors, CI/CD, and issue trackers round out the core stack.

Adoption by tool category, tracked 2018-2021. Source: State of Developer Nation

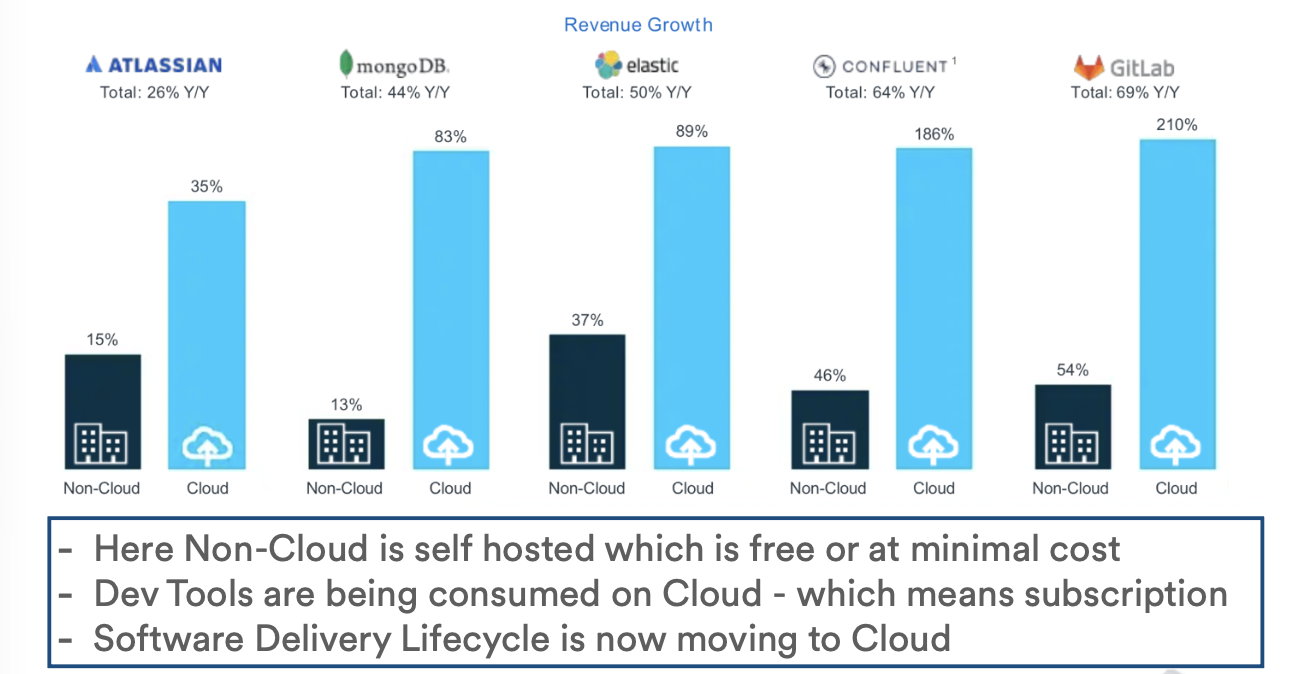

The interesting question isn't what they use -- it's why they're paying for it. Cloud changed the model. Non-cloud is self-hosted, free or minimal cost. Cloud-native means subscription. And the Software Delivery Lifecycle has decisively moved to cloud.

Cloud revenue consistently outpacing non-cloud across every major dev tool company. Atlassian +26%, MongoDB +44%, Elastic +50%, Confluent +64%, GitLab +69% YoY.

The reason they're not free: inability to build internal tools. Developers at 50-person companies aren't going to roll their own CI/CD, observability stack, or API gateway. They subscribe. And once subscribed, they stay.

How much do they earn and retain?

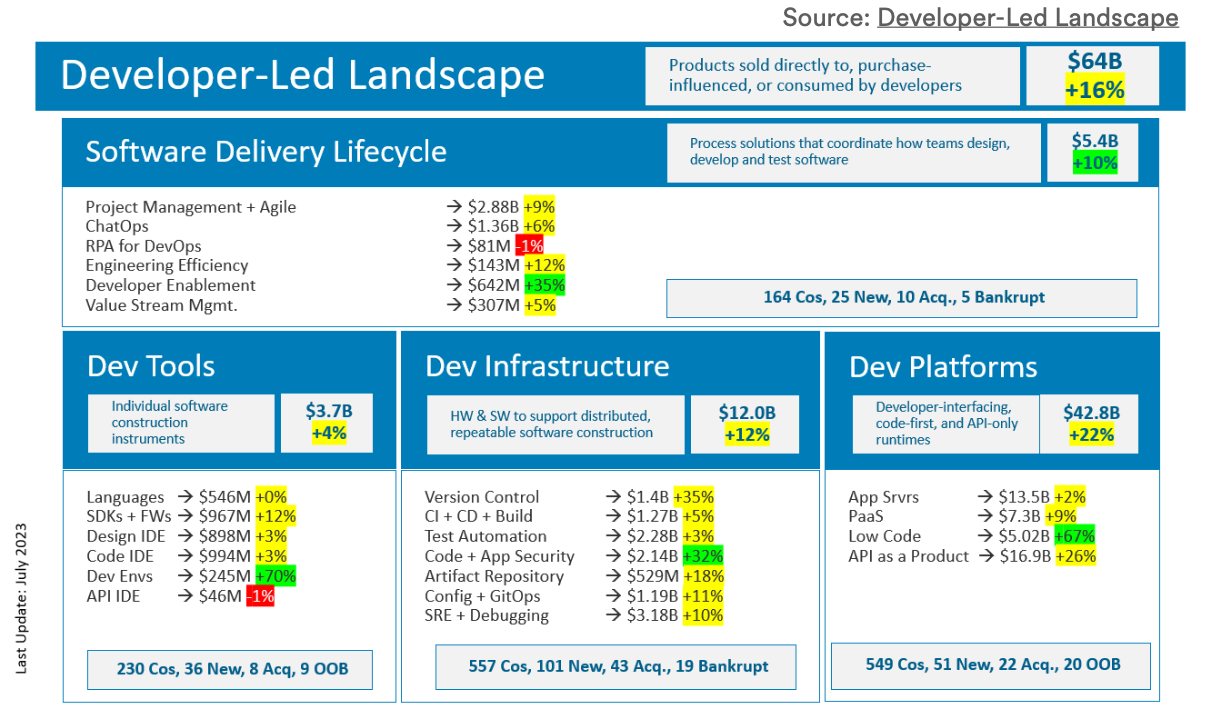

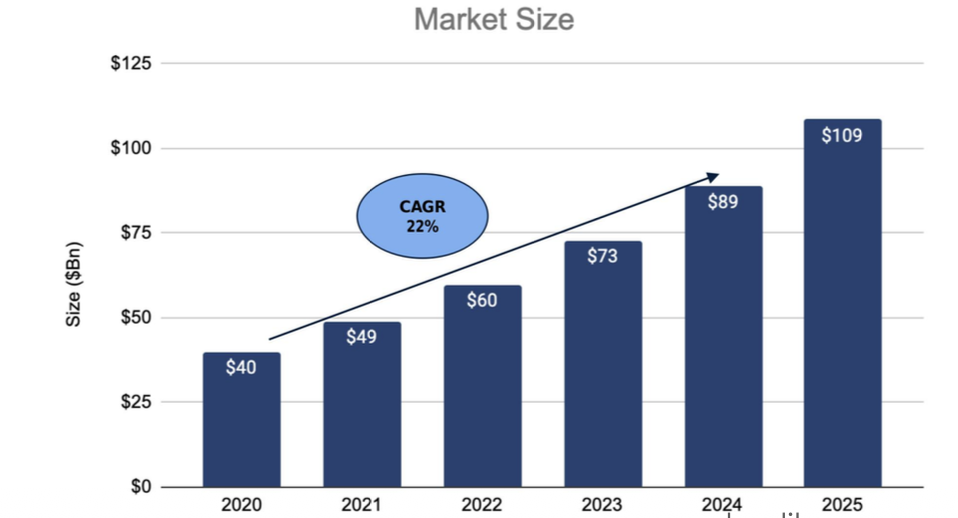

The developer-led landscape is a $64 billion market. At 22% CAGR, projected to reach $109 billion by 2025.

Dev Platforms at $42.8B (+22% YoY) is the largest and fastest-growing segment. Dev Infrastructure at $12.0B (+12%), Dev Tools at $3.7B (+4%). Source: Developer-Led Landscape

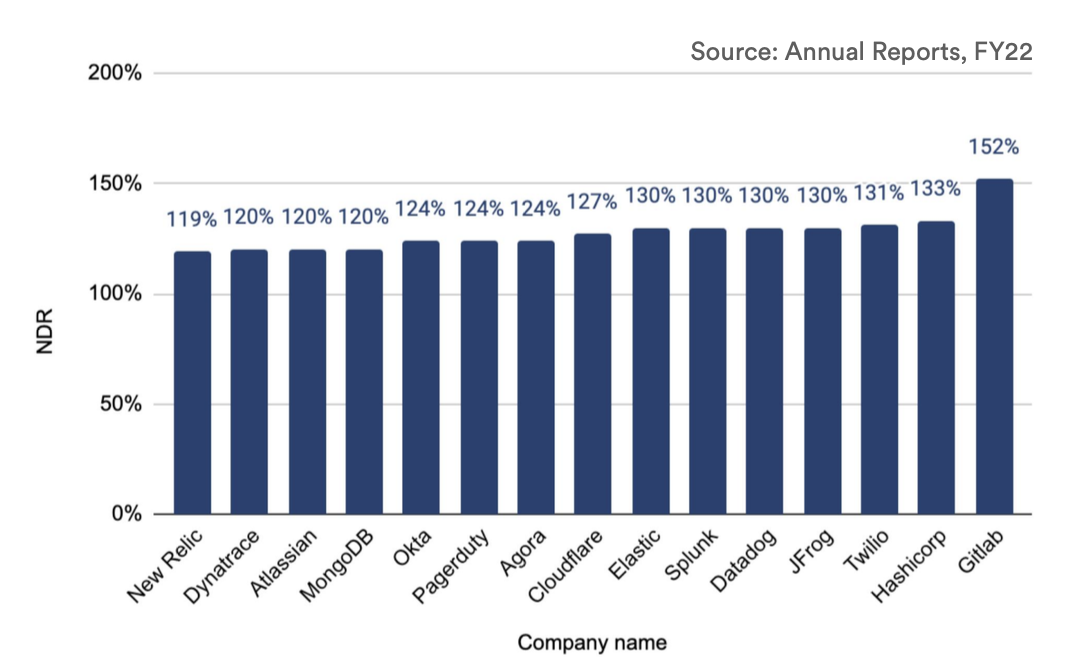

The retention numbers are what make this attractive. NDR across public dev tool companies averages 125%+. Every company in the chart above 119%, several above 130%, GitLab at 152%.

Land with one team, expand across the org as usage grows. No re-selling required. Source: Annual Reports, FY22

The ecosystem and emerging themes

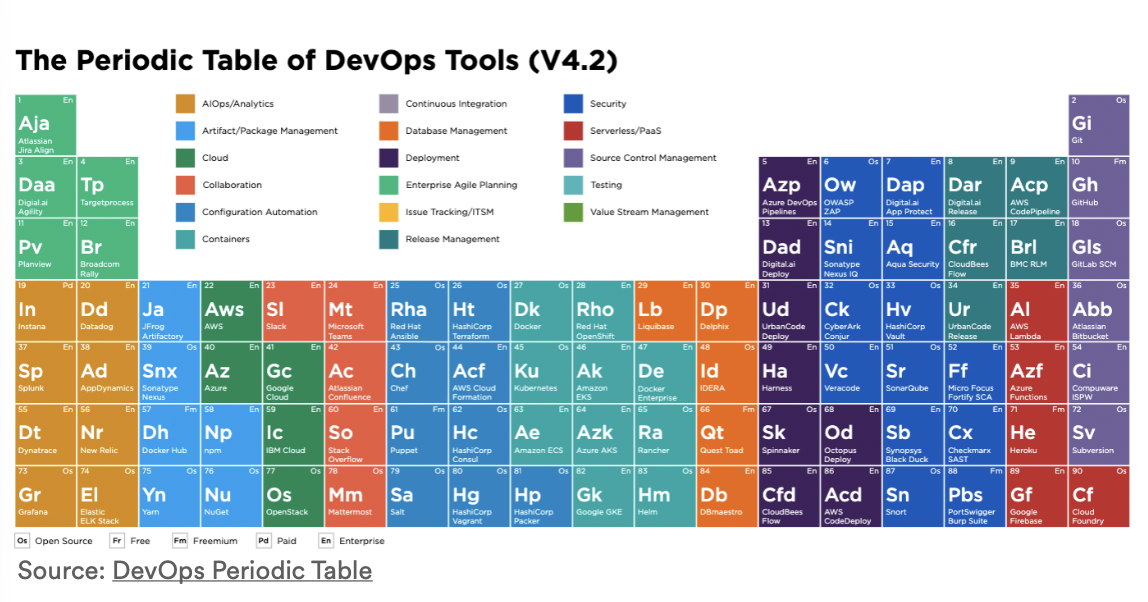

The DevOps Periodic Table maps 22 distinct segments across AI/Analytics, Containers, CI, Deployment, Security, Testing, and more.

Open source dominates most segments as the baseline. Enterprise tools lead on features, which is how they justify paid plans. Segment crowding is real -- most categories have 50+ companies. Source: DevOps Periodic Table

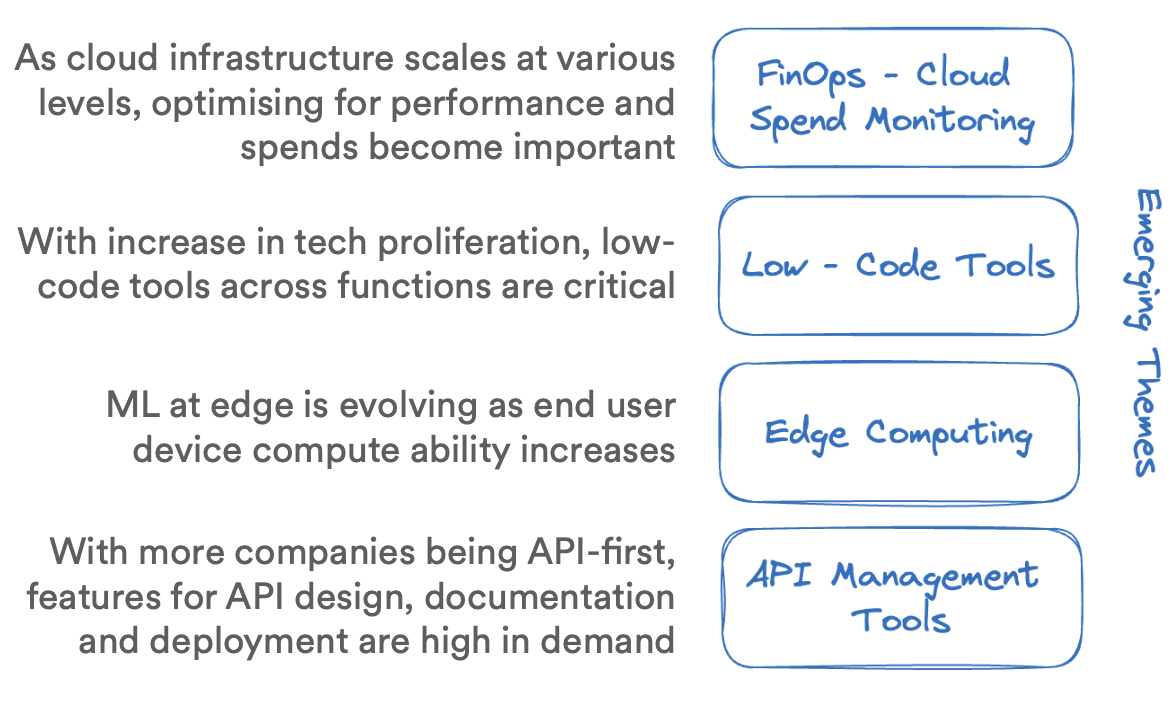

From those 22 segments, four themes stand out as high-growth vectors:

FinOps - Cloud spend monitoring

Cloud infrastructure spend is now a P&L line item, not just an engineering concern. FinOps emerged as a discipline to forecast, monitor, and optimise that spend -- typically reported to CTOs but increasingly with CFO attention.

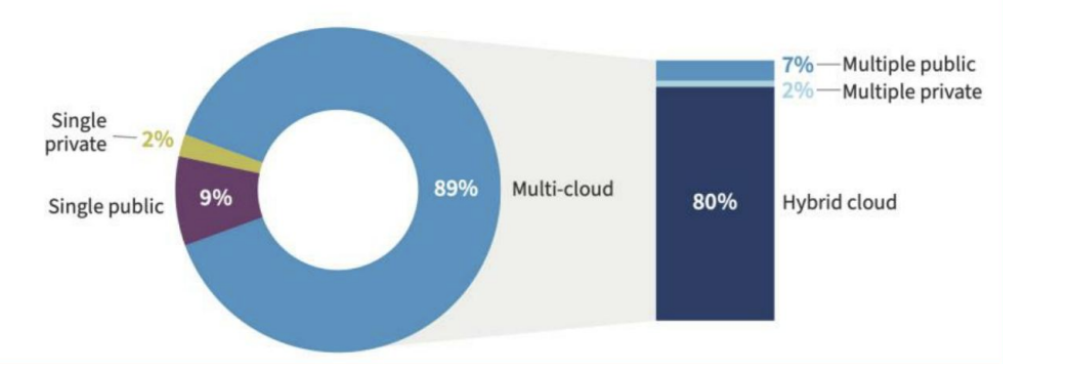

89% multi-cloud adoption means no single CSP's native tools are sufficient. That gap is where CloudQuery, Lumigo, Finout, and Splunk sit. The problem gets worse as cloud adoption deepens, not better.

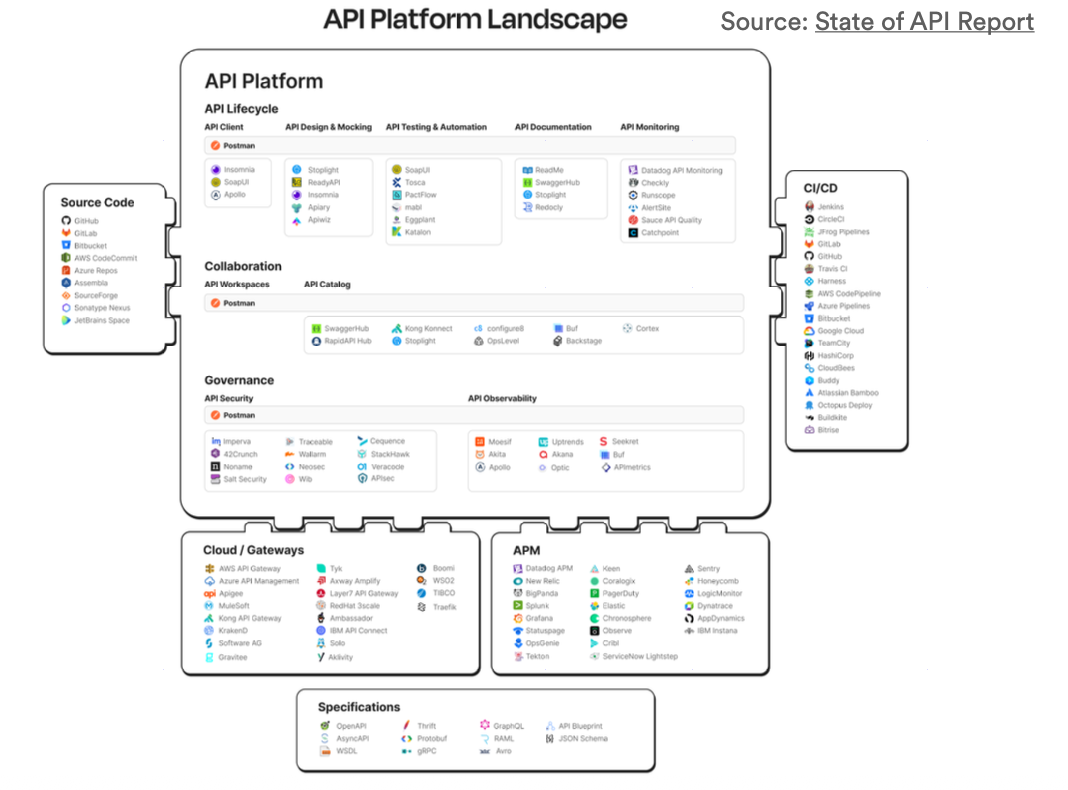

API Management

More companies are going API-first. Many are monetising via API-as-a-product. API design, development, testing, security, and documentation stops being an afterthought and becomes a core product function.

Source: State of API Report

Three emerging patterns in this segment:

- Universal API management across the full enterprise stack

- In-built security testing as part of the API lifecycle

- API discovery and auto-documentation -- as API sprawl grows, knowing what you have becomes a problem

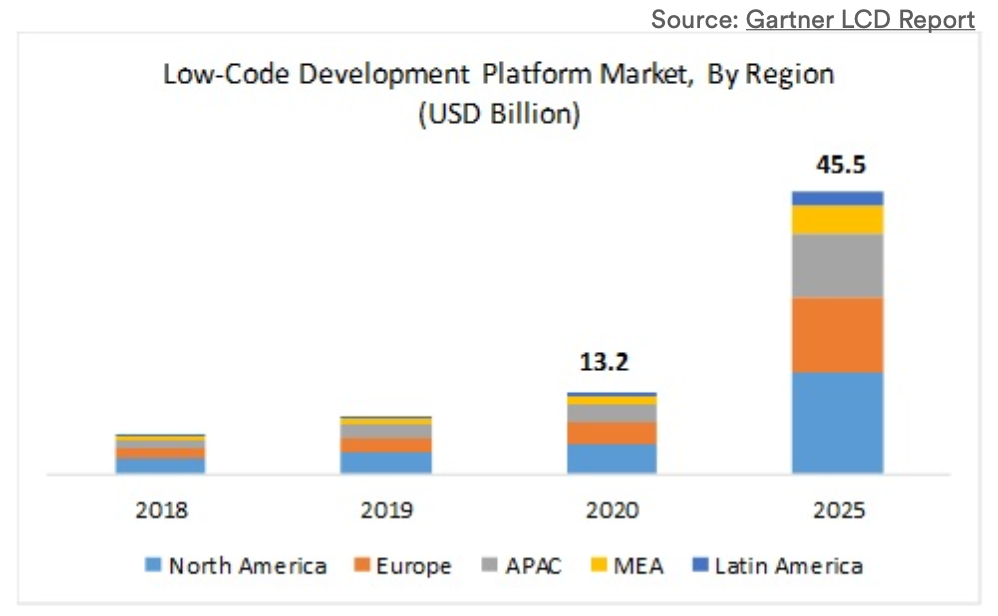

Low Code Tools

Low-code is the developer tool category that's actually not for developers -- it's for everyone else. As organisations try to enable non-technical employees to build and maintain applications, low-code platforms sit between SaaS and custom engineering.

23% annual growth rate. From $1.5B in 2018 to a projected $45.5B by 2025. North America leads, APAC accelerating. Source: Gartner LCD Report

Freemium or per-user/per-application pricing makes adoption frictionless -- teams can start without procurement. Players: Quickbase, OutSystems, Retool, Bubble.

Edge Computing

Edge computing brings computation and data storage closer to where data originates, rather than routing back to a central cloud region. Most valuable for event-driven applications where latency is the bottleneck.

The tailwinds: 5G rollout, increasing end-user device compute capability, ML-at-edge reducing privacy concerns, automation enabling edge deployments to scale. Players: Macrometa, Stackpath, SiMa.ai. This segment is the earliest of the four -- infrastructure-level bets where the category is still forming.

What this means

The developer tool market is not a niche. $64 billion, growing at 22%+ CAGR, with retention metrics that most SaaS categories can't touch.

The structural reason: developers are the new procurement unit. They choose tools bottom-up, spread them inside organisations. Once a tool is embedded in the development workflow -- in the CI/CD pipeline, the monitoring stack, the API gateway -- it's genuinely hard to rip out.

The four themes above each sit at an intersection of that structural shift with a specific forcing function: cloud cost pressure, API-first architecture, non-technical users, 5G and compute. Each is large enough to support multiple winners.

This deck was an early attempt at mapping it. The landscape has moved since -- AI-native tooling has reshaped several of these categories -- but the underlying logic holds.